Spring In the Trap

Spring has sprung – the daffodils stand tall, blossom trees proliferate and the pussy willow springs into languid attention. However, […]

Spring has sprung – the daffodils stand tall, blossom trees proliferate and the pussy willow springs into languid attention. However, […]

In this Rogue Rant, I take aim at the controlled opposition which is headed-up by Rupert the Bare Lowe, Nigel

Sleuth Investigation Conclusively Demonstrates That the Financial System is Credit-based and that Any and All Loans are Illusory. This essay

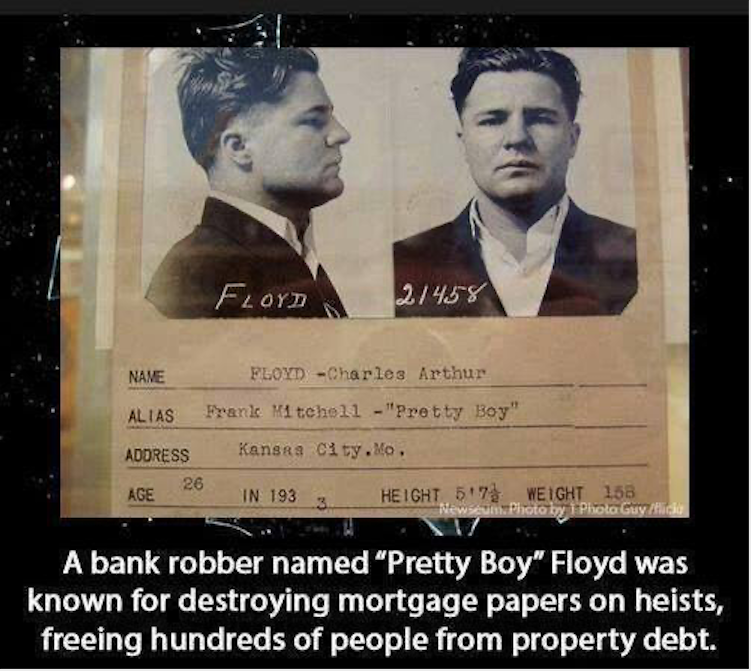

The Shekels or the ‘money’ is a chimera that many chase. It is a falsity on the simple basis that

How on earth did I come to this? An overview of a journey that began in Huddersfield and led to

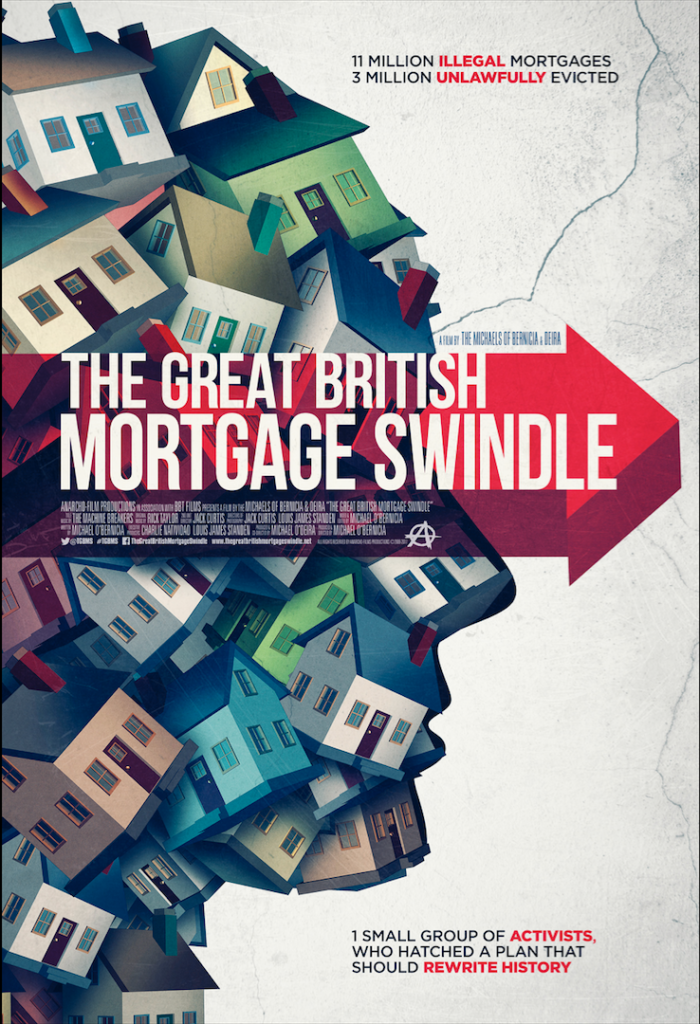

Built on an already fraudulent monetary system. Here is why they are doomed to failure. The puppet criminal government of

A Deep Dive into Money and the Fake Financial System Regular readers and listeners will be well-aware that money is

What follows is a redacted account of how a False Lender, in this case, the Defendant (D) the Nationwide Building

In May, 2019, Michael O’Bernicia and yours truly were interviewed by Ross Ashcroft at the Renegade Inc Studio in London.

Under whose Authority Do You Stand? The ‘UK Establishment’ is firmly and deliberately embedded in the ‘Legal’ system, meaning they