A Rogue Rant

In this Rogue Rant, I take aim at the controlled opposition which is headed-up by Rupert the Bare Lowe, Nigel […]

In this Rogue Rant, I take aim at the controlled opposition which is headed-up by Rupert the Bare Lowe, Nigel […]

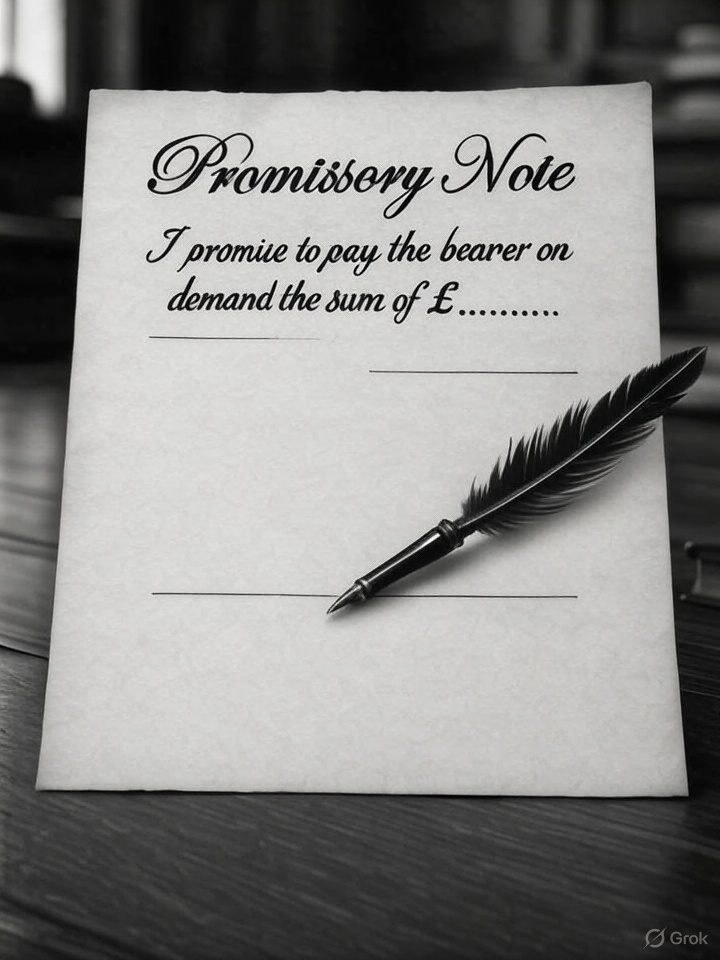

A friend recently tendered, in good faith, a promissory note to the CEO of Nationwide Building Society to settle and

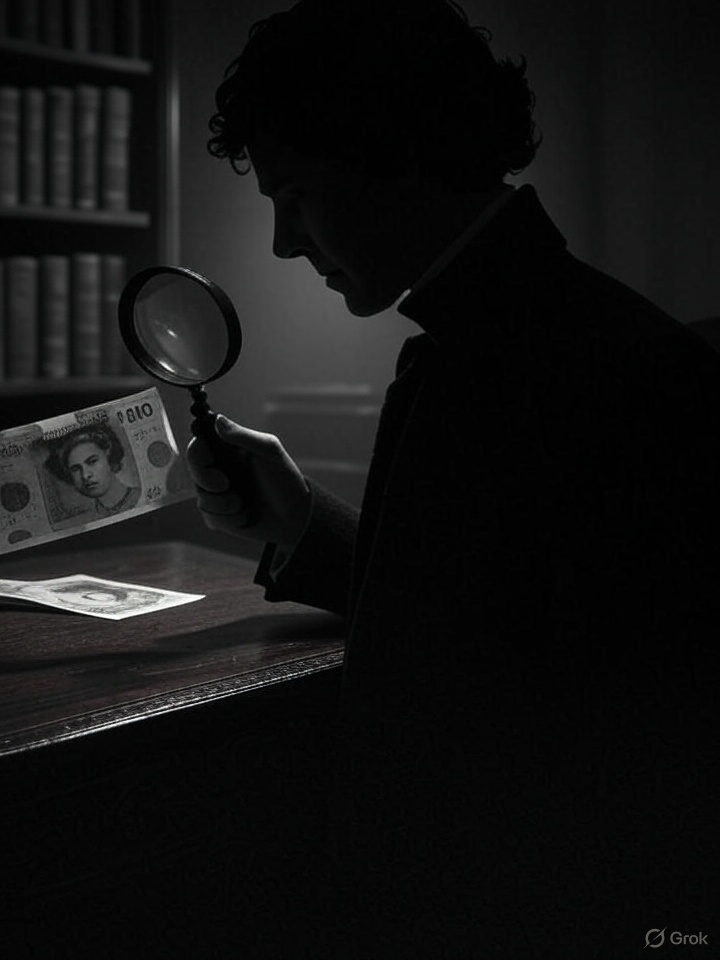

Sleuth Investigation Conclusively Demonstrates That the Financial System is Credit-based and that Any and All Loans are Illusory. This essay

Plainly expressed, the Truth is simple, which is in marked contrast to the falsehoods that are so manifestly pumped out

Credit creation and the Deception of Banking. In this ramble through the woods adjacent to Beauvale Priory, in Nottinghamshire, I

The inherent honour of making a promise is that the individual should fulfill it. By tendering a valid form of

Consensus Reality is a phrase that means those sets of things which the majority of people consider to be real.

The notorious Bradford and Bingley Building Society (now known as UKAR), who were bailed out to the tune of

The Rothschilds, their Polipuppets and the Fraud of the General Election Let’s face facts – the ‘snap’ election scheduled for

The Immorality of Banking – a plain tale Of Old King Coal, fake LOBO loans and illusory debt, exposed to