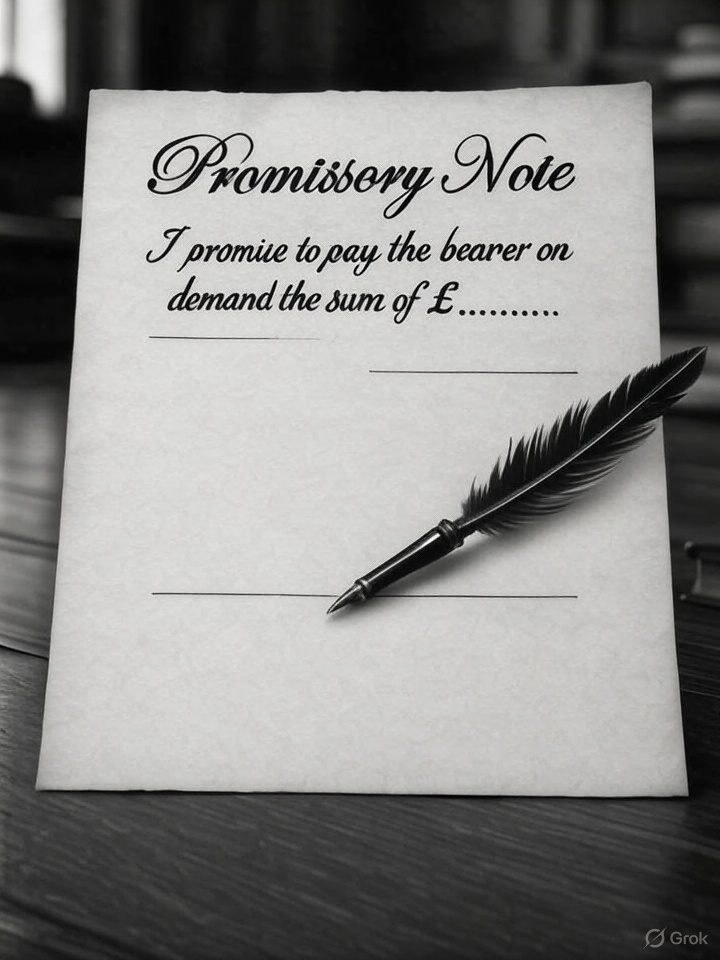

The Promissory Note

A friend recently tendered, in good faith, a promissory note to the CEO of Nationwide Building Society to settle and […]

A friend recently tendered, in good faith, a promissory note to the CEO of Nationwide Building Society to settle and […]

The Great British Mortgage Swindle in Real Time. This Rogue Cast (070) is a condensed exposition of the various components

Plainly expressed, the Truth is simple, which is in marked contrast to the falsehoods that are so manifestly pumped out

Credit creation and the Deception of Banking. In this ramble through the woods adjacent to Beauvale Priory, in Nottinghamshire, I

The inherent honour of making a promise is that the individual should fulfill it. By tendering a valid form of