THE TRUTH RULES, OK?

SHADOW PLAY: THE UNREALITY OF ‘HER MAJESTY’S COURTS’

It is an absolute disgrace that families are being evicted from their homes in spite of the fact that there is no valid deed and no debt owed (because no loan ever existed). The abhorrent nature of it all is further compounded when these and other salient facts are brought up in ‘Court’ and wilfully ignored by the ‘judge’. When families are evicted without there ever being a valid warrant, signed and authenticated by the presiding ‘judge’ and when said warrant shows no moneys are actually owed and when extreme violence is perpetrated on the individuals who stand up to the tyranny, then one has to ask the reasonable question:

is it really a court and is the judge really a judge or simply an actor, bought and paid for by the banking fraternity?

Due process of the law guarantees a fair hearing. In Britain, all possession hearings begin in the local County court. It is now almost 7 years since RM stepped into defend himself against a fake possession claim made by the Bradford and Bingley against his home of 16 years. He did not step into the courtly theatre unprepared – he had a notarised Affidavit of Obligation (commercial lien) and a counter claim. Thus, the facts of the matter had been established before he went in:

- There was no evidence that a loan had been made.

- The bank had used his promise to pay to create the credit and there was no evidence to suggest otherwise.

- He had already paid, from his sweat equity, some £67k to the bank on an fake debt of £34k, almost twice what the bank falsely claimed to have ‘loaned’ him.

- There was no valid mortgage deed – therefore, there was no mortgage.

- Thus, there was no evidence that he had not been defrauded.

This commercial lien proved that he had gone to great lengths to resolve the matter and the facts had been lawfully determined and witnessed by the Public Notary who had duly executed a Notice of Default.

The facts of the matter were established in court and a counter claim had been issued against the bank.

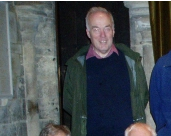

When he presented these reasonable facts to a man called Richard Inglis (below, left) who was acting as ‘judge, jury and executioner’, that man had a duty of care towards him which meant he could not ignore the reasonableness of what was presented to him.

After all, if there was no evidence any loan had taken place, then how could a (suspended) possession order be granted?

And yet, Richard deliberately ignored these facts, just like all the other judges who preside in said courts do.

At that time, the court documents were stamped with the seal of ‘Nottingham County Court’ .

By ignoring the facts of the matter, and siding with the false testimony of a ‘legal officer’ that a debt was owed, he showed himself to be biased.

Up until the second world war, all county court hearings were before a jury. This was suspended during war time and never reinstated.

RM is firmly of the view that had the matter been heard before a jury of his peers, then no possession order would have been issued.

So, why did Richard, the ‘judge’, rule against him? It could not be that the defence was unreasonable – it was based in fact, logic and reason and demonstrated beyond reasonable doubt that the mechanics of banking and credit creation meant no loan had ever taken place.

Yet, Richard completely ignored these facts.

If he did not understand the facts about the creation of credit, then he was incompetent to preside. On that basis, an application was made to set aside his possession order. After all, it was void on the ground he had ignored the facts of the affidavit. Richard dismissed that application too.

If he was unable to grasp the mechanics of the loan, then he was not fit to preside.

He showed himself to be blatantly biased in that he accepted the false testimony of a third party that moneys were actually owed.

Why would he do that? There are at least five possibilities:

- He had a vested interest in continuing TGBMS.

- He had been bribed or received a kickback to find in favour of the bank and defeat any defence made by a litigant against a bank..

- He was truly incompetent to the point of not being able to understand the reality of how a mortgage is created.

- He had sworn a ‘mafia’ oath to the Privy Council which meant he literally could not hear any criticism or allegations against a Crown entity, such as a registered and licenced credit creator, like the B&B.

- He was being bribed by some hidden hand who had something scandalous on him.

- Having routinely issued hundreds of possession claims down the years, he did not have the courage to strike out the bank’s claim and find against them as it would mean all his other ‘rulings’ had been void.

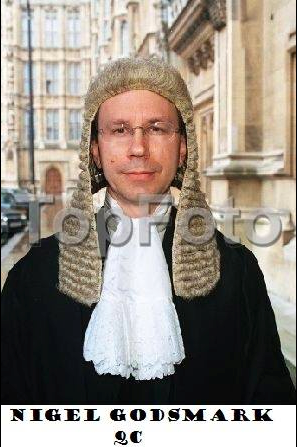

In any event, following another unlawful eviction on 07 November, 2011 when Richard unlawfully ordered the riot police (below), without a warrant, to batter open a gate and crowbar their way into the home where RM was living after the first eviction of 04 November, 2010, he and the court were served with a Notice of Lien interest, said man was removed from his role as senior judge at Nottingham (a role now occupied by Nigel Godsmark). This was no mere coincidence and followed his being ‘reported’ to the Archbishop of Canterbury for ignoring the aforementioned notarised affidavit (Notary publics operate under the aegis of said bishop).

During the subsequent years I have witnessed at first hand many judges act in this illogical and cowardly way. In particular, Richard’s successor at Nottingham, Nigel (left), springs to mind in the matter of the same bank (Bradford and Bingley) vs Tom Crawford, when on 01 May, 2015, in clear contradiction of the facts, he ruled in favour of said bank and ‘lifted’ the stay on a non-existent warrant for possession.

Is cowardice the problem? Could it be that none of these judges has the balls to do the right thing and rule in favour of the mortgagor? Has someone, somewhere got something on these judges?

Right now, it appears to RM that there is in fact a shadow court system operating across these lands, that the not-so-hidden hand of Rothschild has taken over. Consider this: all county court stamps now state ‘The County Court’, not the name of the individual court.

Claims are directed through a centralised location in Salford, Greater Manchester.

All orders are now stamped ‘The County Court’ – but what is that supposed to mean? Which County Court? Could it be a shadow court system is currently operating in order to further vet any and all claims that are made against the agencies of the state?

As the forthcoming film, TGBMS reveals, judges across the Isles of Britain are selectively applying the law in favour of the establishment and completely disregard precedents of the High Court in order to rule against any mortgagor who has the temerity to challenge any and all illegal possession claims.

Yet when the matter spills over to the Criminal Courts, where the onus is on the evidence and not mere bias, the facts speak for themselves. As was established in the Crown Court, Leicester there is never a valid warrant for possession. Why is this the case? Why will no judge put his signature on a warrant for possession? Could it be because the claim and the ‘Court’ are bogus?

Could it be because there was never a valid mortgage due to the on-its-face defects of the mortgage deed, the lack of consideration, the failure to disclose how the credit is created on the back of the hypothecated promise to pay and, of course, the fact that there is no valid contract, signed by both parties, as required at law.

The Great British Mortgage Swindle is a multi-leveled fraud, perpetrated on the people by the banks and the authorities who are controlled by the fake religion of Money.

As someone so succinctly put it,

A lie can be half way round the world whilst the truth is still lacing up its boots.”

Seven years on, and in spite of the establishment’s attempts to cover it up, the truth is coming out.

RM’s claim, founded in truth, has not gone away. He remains as entitled to have the fake charge removed by the Land Registry as when he first applied for it in October, 2009, only for it and subsequent applications for the same, to be rejected by the Land Registrar in Nottingham.

To repeat: the truth will out. Seven years on and there are now legal precedents in support of the claims that he was making then, prior and subsequent to the criminal evictions RM suffered in 2010 and 2011:

Bank of Scotland plc v Waugh & Others [2014] established:

A mortgagor is not estopped from relying on the defects in the mortgage deed, which will be void if it does not comply with the provisions of section 1(3) of the LPMPA 1989”; and,

‘the Powers of Attorney clause in the Standard Mortgage Conditions is unenforceable without a stand-alone Powers of Attorney deed, which must be signed by the mortgagor and comply with the Powers of Attorney Act 1971.’

The binding authority of Scott v Southern Pacific Mortgages & Others [2014] UKSC 52 established the irrefutable fact that:

a mortgagor has no rights to grant before the completion of the sale and purchase of the property concerned; hence the instruction that the deed must bear the same date as the transfer of credit to the mortgagor, in order to give the false impression that section 1(3) of the 1989 Act has been complied with. In said case, Lady Hale stated this point most plainly:

“The purchaser was not in a position either at the date of exchange of contracts or at any time up until completion of the purchase to confer equitable proprietary,” and,

“This case has been decided on the simple basis that the purchaser of land cannot create a proprietary interest in the land, which is capable of being an overriding interest, until his contract has been completed,”

And, of course, In the absence of a stand-alone Power of Attorney Deed, which had to be executed by the mortgagor in accordance with the Powers of Attorney Act 1971, any Bank’s Power of Attorney clause in its Standard Mortgage Conditions is legally unenforceable.

It’s been a long 7 years that RM has endured as a direct consequence of the lies and denials of justice perpetrated by a coterie of judges, bailiffs and officers at the Land Registry but he has kept the faith that the truth will out.

TGBMS’ imminent release will serve to bring the facts to the public at large.

https://www.youtube.com/watch?v=ogUZ6QCgoUY

Many lessons have been learned these last 7 years but the most powerful is this: the Truth will ultimately triumph:

FOOTNOTE: Blessings to all and special thanks to the inspiration of John W and Michael of Bernicia and all those brave souls who have stood up in the name of truth to the most pernicious of deceits, The Great British Mortgage Swindle.

As ever, if the reader appreciates the work of RogueMale and is able to make a donation, of whatever size, then he or she is encouraged to do so. Many thanks to all supporters, whoever and wherever they may be.