Revisited: The Tom Crawford Affair

The notorious Bradford and Bingley Building Society (now known as UKAR), who were bailed out to the tune of […]

The notorious Bradford and Bingley Building Society (now known as UKAR), who were bailed out to the tune of […]

Make no mistake, when a small group of determined individuals stand up to tyranny, there is an effect. 8

CUI BONO? The agent provocateur’s purpose is to cause disruption. Divide and Rule is the well-established modus operandi of those

HOW AND WHY THE SO-CALLED MONARCHY – THE QUEEN, ‘REGINA’, THE ‘CROWN’, ‘ROYALTY’ & ALL ASSOCIATED LEGISLATION FOR THE LAST

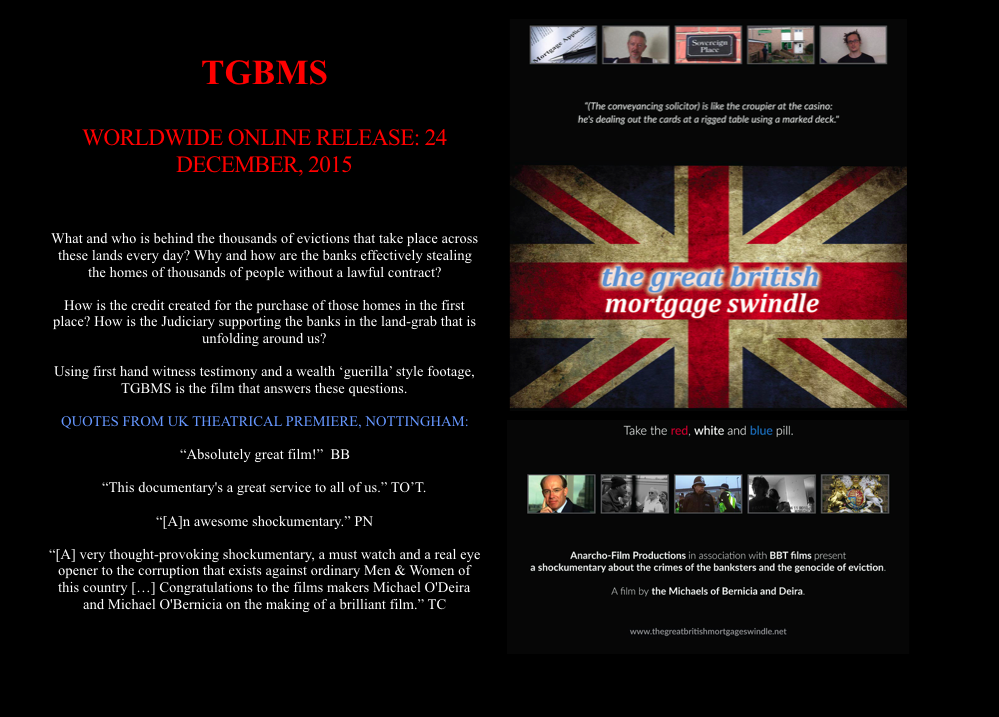

#TGBMS: How institutionalised mortgage fraud is the hot issue of our times. A comparison of a grass roots independent British

NOT GUILTY CASE AGAINST THE ‘ROOF TOP SIX’ + 1 COLLAPSES NO EVIDENCE NO VALID POSSESSION ORDER OR WARRANT EVICTION

NOW AVAILABLE ACROSS THE EARTH – THE FILM THE BANKSTERS & JUDICIARY DON’T WANT YOU TO SEE. The producers

RM answers a dozen questions concerning #TGBMS, The Great British Mortgage Swindle, the new trailer for which is featured below.

The facts of the matter are plain for anyone with a functioning brain: In common usage, theft is the taking