#TGBMS – Knocking Down the Dominoes of Dogma

Defeating dogma has never been easy. On many occasions, the individual can become disheartened that his efforts appear to have […]

Defeating dogma has never been easy. On many occasions, the individual can become disheartened that his efforts appear to have […]

Make no mistake, when a small group of determined individuals stand up to tyranny, there is an effect. 8

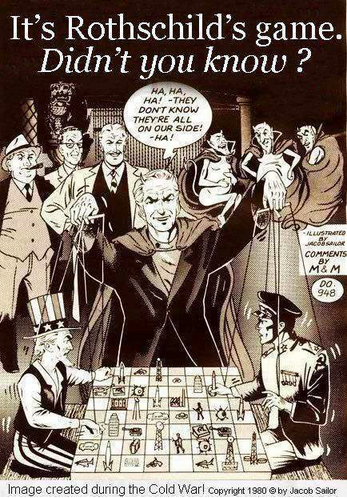

The Rothschilds, their Polipuppets and the Fraud of the General Election Let’s face facts – the ‘snap’ election scheduled for

The Immorality of Banking – a plain tale Of Old King Coal, fake LOBO loans and illusory debt, exposed to

CML REVEAL ONE MILLION BRITISH PEOPLE GENOCIDED BY EVICTION SINCE 2008. #TGBMS – HOW LONG BEFORE THE BRITISH MIDDLE CLASSES

THOSE WHO FLOUT THE RULE OF LAW OR THOSE WHO INSIST ON IT BEING APPLIED? The inherent extremism of the

THE RISE & FALL OF THE WHITE COLLAR CRIMINAL Separating the Image from the Reality. From 26 August 2009 and

Could ignorance ever really be bliss?

If voting made any difference they wouldn’t let us do it.” – Mark Twain Anyone who believes that elections are

How do two films on mortgage fraud compare? One had a budget of $8m, the other zero. Which deals with